Global Trends – Trump 2.0

Imposition of trade tariffs: Historically, during Trump’s first term (2017-2021), trade tensions led to a 7.3% contraction in global trade volume (WTO data) and a drop in manufacturing PMIs worldwide. The Trump administration has already reinstated tariffs on Chinese imports worth $300 billion, with further hikes expected.

Strengthening US Dollar: A hawkish Federal Reserve stance, coupled with increased fiscal stimulus under Trump, has contributed to US dollar appreciation against major global currencies. The Indian Rupee (INR) has depreciated from ₹81/USD to ₹86/USD over the past six months due to capital flight. The US 10-year Treasury yield has crossed 4.5%, making risk-free US assets more attractive, further pressuring EM equities.

Foreign Portfolio Investment (FPI) Outflows: India has seen FPI outflows of Rs. 1 lakh crore in the past three months due to rising US yields and a stronger dollar. Sectors most impacted: Financials and Oil & Gas. Despite FPI outflows, Domestic Institutional Investors (DIIs) have absorbed ₹90,000 crore in inflows YTD, cushioning market volatility.

Indian Economy – Budget 2025

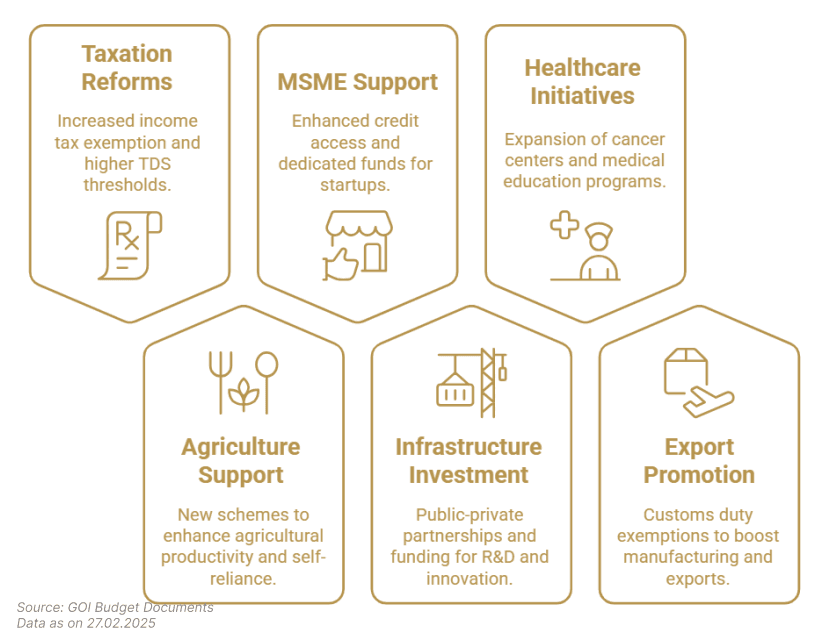

The Union Budget included measures aimed at boosting domestic demand, key initiatives include:

Slashing personal tax rates

Infrastructure Development: enhanced funding for infrastructure projects, particularly in manufacturing, textiles, and electronics

Renewable Energy and Clean Technology: A new initiative focuses on achieving 500 GW of renewable energy capacity by 2030

Electric Vehicles (EVs): The budget removes Basic Customs Duty on critical minerals such as cobalt, zinc, lead, and lithium-ion battery components.

Reforms to support Micro, Small, and Medium Enterprises (MSMEs)

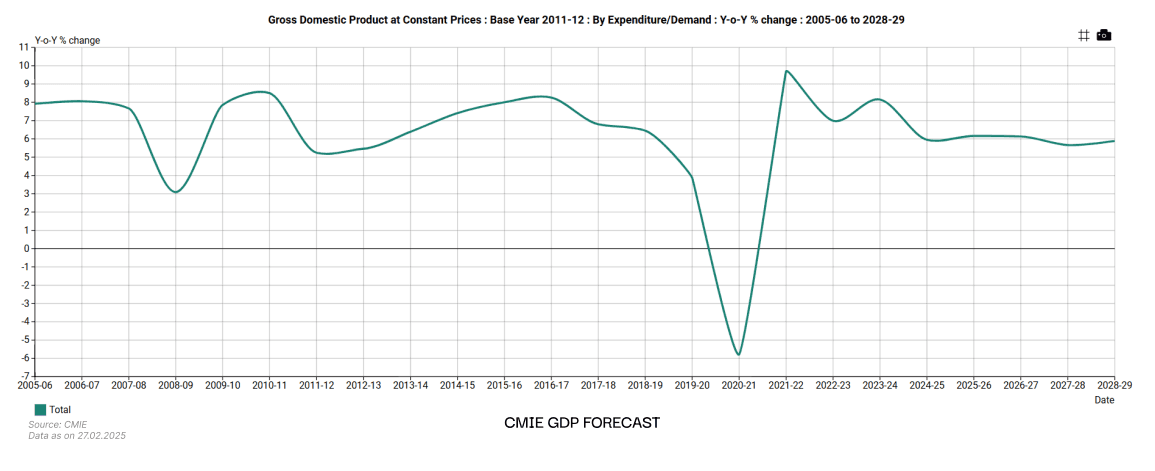

The Reserve Bank of India (RBI) anticipates that these measures, combined with increased rural demand, tax relief and rate cuts will boost urban consumption. The RBI projects GDP growth to improve to 6.6% in the January- March 2025 quarter, with an annual forecast of 6.7% for 2025-26. Inflation is expected to ease to 4.2% in the next financial year, supported by these budgetary measures. The focus on infrastructure, renewable energy, and EVs is likely to attract private investments, enhance manufacturing capabilities, and create employment opportunities, contributing to overall economic resilience.

Indian Economy – RBI Interest Rate cuts

In February 2025, the Reserve Bank of India (RBI) reduced the repo rate by 25 basis points, bringing it down from 6.5% to 6.25%. The reduction in the repo rate directly influences borrowing costs for both individuals and businesses. Following the RBI's decision, several banks, including the State Bank of India (SBI) and Punjab National Bank (PNB), announced reductions in their lending rates. The central bank's models project an improvement in GDP growth to 6.6% for the January-March 2025 quarter, up from 5.4% in the previous quarter. Inflation is expected to ease to 4.2% in the upcoming financial year.

Equity Markets

GDP to Market Capitalisation: India's share of the global market capitalisation currently stands at 3.63%, an 18-month low, down from 4.52% in September 2024. Meanwhile, India's share of global GDP at current prices has reached an all-time high of 3.5%. Historically, the country's market capitalisation has grown in line with GDP, with its global market cap share generally remaining below its GDP share. In previous instances where India's market cap share exceeded its GDP share, such as in 2012-13, it was followed by a period of correction.

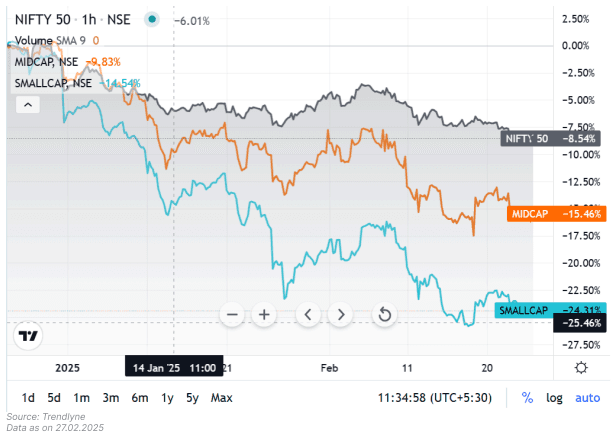

Market Corrections: Year to Date, markets have undergone a significant correction due to FPI outflows and lukewarm Q3 Corporate Earnings, with major indexes based on market capitalisation declining from their peak levels. The MidCap and Small-Cap segments have borne the brunt of this downturn, as they were widely considered overvalued.

Systematic Investment Plans (SIPs): Despite an increase in systematic investment plan (SIPs) contributions from 2020 to 2025, the stoppage ratio of SIPs, which stood at 52.3 per cent last year, spiked to 109 per cent in January 2025. Against 56.19 lakh new SIPs registered, 61.33 lakh were discontinued last month. This means more SIPs were discontinued in January 2025 than new ones started, reveals the latest Association of Mutual Funds in India (AMFI) data.

Corporate Earnings: Subdued Quarter 3 Earnings Results for FY24-25 contributed to the market correction seen year to date in the Indian equity markets, with over 50% of the companies whose results were published showing negative growth, indicating a slowdown in the corporate sector. While large-cap companies reported stable growth, midcap and small-cap firms faced margin pressures due to rising input costs and market volatility.

Good Time to Invest: Although India's macroeconomic fundamentals are stronger than those of many other countries, overall valuations remain high, with some areas appearing excessively priced. However, in certain sectors, valuations have mean-reverted and are now trading below their historical median multiples.

Fixed Income Markets

Interest and Inflation: With moderating inflation forecasts showing stable inflation in the 4-4.5% range over the next 3 quarters and the recent RBI rate cut, while the Reserve Bank of India (RBI) has maintained a cautious stance, market experts anticipate a potential rate cut of up to 50 basis points in 2025. Such a move could enhance liquidity and drive demand for fixed income securities.

Fiscal Consolidation: The Union Budget 2025-26 sets a fiscal deficit target of 4.4% of GDP, down from the revised 4.8% for the current year. This commitment to fiscal prudence is expected to positively influence the fixed income market by potentially lowering bond yields and stabilising spreads.

India Bond Yields and Spread: The benchmark 10-year government bond yields have stabilised between 6.7% and 6.9% over the past year, reflecting a balanced demand-supply dynamic. Indian banks have raised a record ₹892 billion through infrastructure bonds this financial year. However, the increased supply has led investors to demand higher returns, resulting in wider spreads between corporate and government bond yields.

Gold

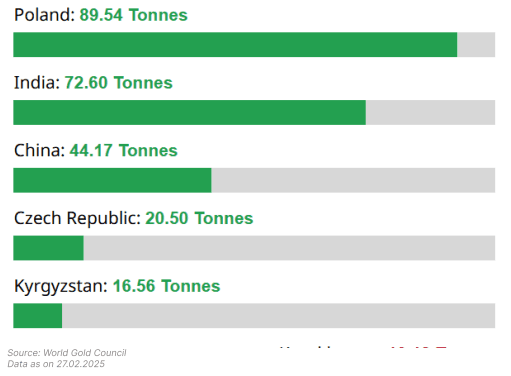

Rising Gold Prices: Gold prices have reached an all-time high, with spot prices nearing $3,000 per ounce mark. This surge is primarily driven by escalating geopolitical tensions, notably between the U.S. and Ukraine, and the implementation of new U.S. tariffs on major trade partners, including Canada, Mexico, and China.